Blank Promissory Note Form for the State of Iowa

Blank Promissory Note Form for the State of Iowa

Iowa Transfer on Death Deed - This form allows for clear, legal documentation of one’s end-of-life property wishes.

Iowa Trailer Bill of Sale - Validates the completion of a trailer sale agreement.

For anyone looking to navigate the intricacies of property transfer, our guide on the necessary Alabama bill of sale documentation can be invaluable. For more detailed information, refer to the Alabama bill of sale form requirements.

Power of Attorney Attorney - A vital tool for families needing flexible care arrangements for children.

A loan agreement is a document that outlines the terms of a loan between a lender and a borrower. Like a promissory note, it specifies the amount borrowed, interest rates, and repayment terms. However, a loan agreement often includes additional details such as collateral and conditions for default, making it more comprehensive than a standard promissory note.

In the realm of real estate transactions, understanding various forms is crucial, and one such essential document is the Texas TREC Residential Contract form. This standardized form is used in the sale of residential properties and outlines important terms agreed upon by both parties. For more information, visit Texas Documents to ensure you have all the necessary knowledge for a successful transaction.

A personal loan agreement serves a similar purpose to a promissory note but is typically used for loans between individuals. It details the loan amount, repayment schedule, and any interest. While a promissory note is a straightforward promise to pay, a personal loan agreement can include terms that protect both parties, such as what happens if the borrower fails to repay.

A mortgage is a specific type of promissory note that involves real estate. It secures the loan with the property itself. Like a standard promissory note, it outlines the borrower's obligation to repay the loan. However, a mortgage also includes clauses related to foreclosure and the lender's rights to the property if the borrower defaults.

A car loan agreement is similar to a promissory note but specifically pertains to financing the purchase of a vehicle. It outlines the loan amount, interest rate, and repayment schedule. Just like a promissory note, it serves as a legal document that holds the borrower accountable for repayment, but it may also include details about the vehicle being financed.

A business loan agreement is tailored for loans taken out by businesses. It functions similarly to a promissory note by specifying the loan amount and repayment terms. However, it often includes additional provisions related to the business’s financial health and may require personal guarantees from business owners, making it more complex.

An installment agreement is a payment plan that allows a borrower to pay back a debt in regular installments over time. It shares similarities with a promissory note in that it outlines the payment schedule and total amount owed. However, it often includes more detailed terms regarding late payments and penalties.

A demand note is a type of promissory note that can be called in for payment at any time. While it shares the basic structure of a standard promissory note, it differs in that the lender can request repayment without prior notice, making it a more flexible but potentially risky option for borrowers.

A lease agreement, while primarily used for renting property, can have similarities to a promissory note in that it requires regular payments. It outlines the terms of the lease, including payment amounts and due dates. However, it also covers responsibilities related to property maintenance and use, which a promissory note does not.

A credit agreement is a broader document that outlines the terms of a line of credit. It is similar to a promissory note in that it details repayment terms and interest rates. However, a credit agreement may allow for borrowing up to a certain limit and includes terms on how and when the borrower can draw funds.

A student loan agreement is specifically designed for educational financing. Like a promissory note, it details the loan amount and repayment terms. However, it often includes provisions for deferment and forgiveness, which are not typically found in standard promissory notes, reflecting the unique nature of educational financing.

When entering into a financial agreement, particularly one involving a promissory note in Iowa, several other forms and documents may be necessary to ensure clarity and legal compliance. Each of these documents serves a unique purpose, contributing to the overall structure of the agreement. Below is a list of commonly used forms that complement the Iowa Promissory Note.

Utilizing these documents alongside the Iowa Promissory Note can help clarify the terms of the agreement and protect the interests of both parties involved. Understanding each component is crucial for a smooth and legally sound transaction.

When filling out the Iowa Promissory Note form, it is essential to approach the task with care and attention to detail. Below is a list of four important do's and don'ts to keep in mind.

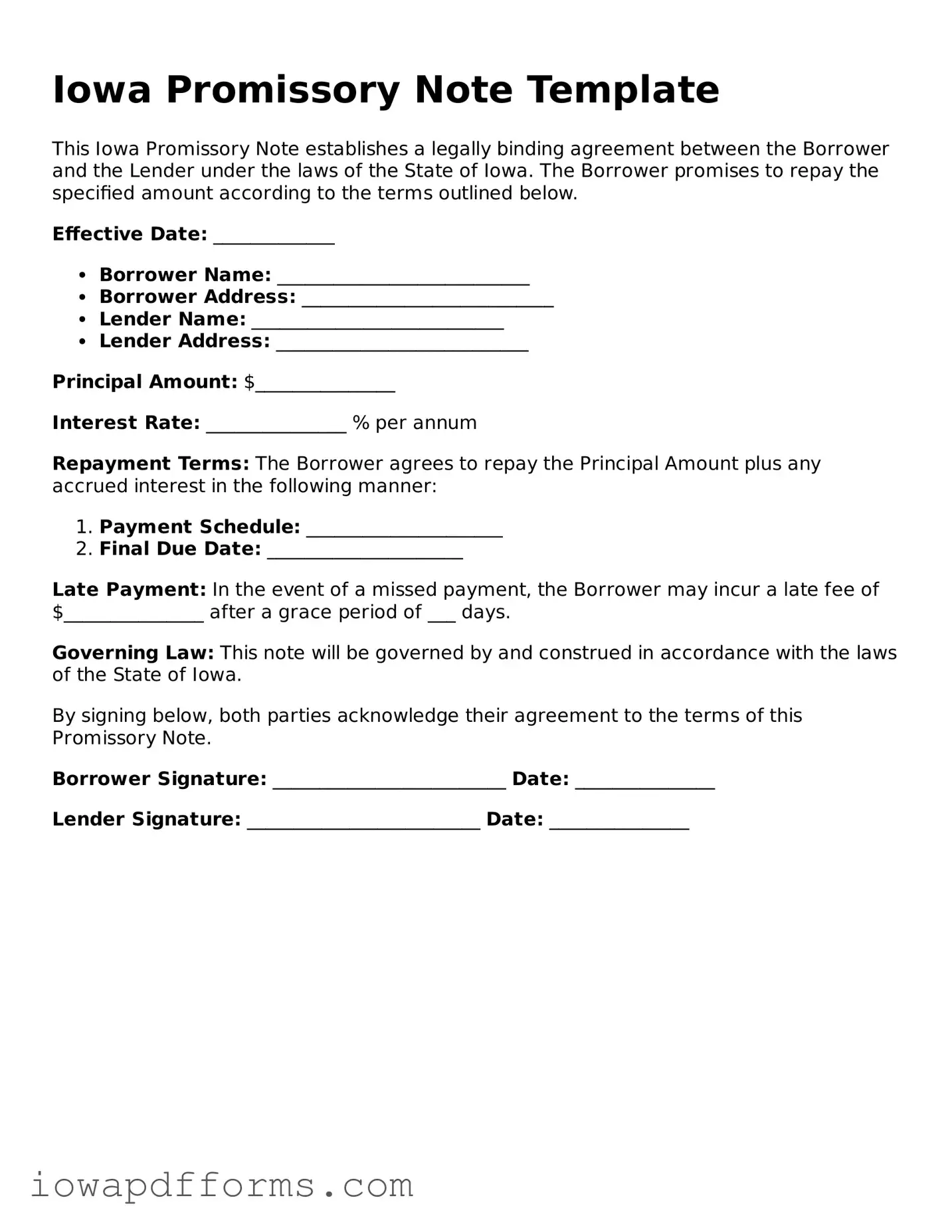

Iowa Promissory Note Template

This Iowa Promissory Note establishes a legally binding agreement between the Borrower and the Lender under the laws of the State of Iowa. The Borrower promises to repay the specified amount according to the terms outlined below.

Effective Date: _____________

Principal Amount: $_______________

Interest Rate: _______________ % per annum

Repayment Terms: The Borrower agrees to repay the Principal Amount plus any accrued interest in the following manner:

Late Payment: In the event of a missed payment, the Borrower may incur a late fee of $_______________ after a grace period of ___ days.

Governing Law: This note will be governed by and construed in accordance with the laws of the State of Iowa.

By signing below, both parties acknowledge their agreement to the terms of this Promissory Note.

Borrower Signature: _________________________ Date: _______________

Lender Signature: _________________________ Date: _______________