Fill in Your Iowa Ia 2848 Template

Fill in Your Iowa Ia 2848 Template

Termination of Parental Rights Iowa - It's essential to verify whether individuals have valid licenses if transportation is required.

In addition to ensuring a smooth transfer of ownership, utilizing the New York Bill of Sale form can also be simplified by accessing resources such as Top Forms Online, where templates and guidance are readily available to help you complete the necessary documentation accurately.

Iowa Divorce Forms - This form is critical for lawful boundaries when facing domestic abuse situations, ensuring safety swiftly.

The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, serves a similar purpose to the Iowa IA 2848 form. Both documents allow taxpayers to designate a representative to act on their behalf regarding tax matters. The IRS Form 2848 requires the taxpayer's information, the representative's details, and the specific tax matters involved. It enables the appointed representative to access confidential tax information and communicate with the IRS on behalf of the taxpayer, ensuring a streamlined process for managing tax obligations at the federal level.

The California Form 3520, Power of Attorney, shares similarities with the Iowa IA 2848 form in that it allows taxpayers to appoint someone to handle their tax affairs. This form is specific to California and requires the taxpayer’s identification and the representative's information. Like the Iowa form, it grants the representative the authority to receive tax information and communicate with the California Department of Tax and Fee Administration. Both forms emphasize the importance of correctly identifying the tax matters involved to ensure effective representation.

The Texas Real Estate Sales Contract form is a crucial document in real estate transactions, which outlines the agreed terms between buyers and sellers in Texas. It specifies vital aspects such as property details, financing arrangements, and closing procedures to ensure clarity and legal compliance. To learn more about this important form, visit Texas Documents for additional resources and guidance.

The New York State Form POA-1, Power of Attorney, is another document akin to the Iowa IA 2848 form. This New York form permits taxpayers to authorize a representative to act on their behalf regarding state tax matters. It requires similar information, including taxpayer and representative details, and specifies the tax types involved. Both forms allow representatives to access confidential information and represent taxpayers in dealings with the respective state tax authorities, highlighting the common goal of facilitating taxpayer representation.

The Florida Form DR-835, Power of Attorney, is comparable to the Iowa IA 2848 form in that it enables taxpayers to appoint someone to handle their tax-related issues. This form requires the taxpayer's information and the representative's details, similar to the Iowa form. It grants the representative the authority to act on behalf of the taxpayer, ensuring that they can manage tax matters efficiently. Both forms emphasize the need for clarity regarding the specific tax issues to be addressed by the appointed representative.

The Texas Form 05-102, Power of Attorney, mirrors the Iowa IA 2848 form by allowing taxpayers to designate a representative for tax matters. This Texas form collects the necessary taxpayer and representative information and outlines the scope of authority granted to the representative. Like the Iowa form, it aims to facilitate communication between the taxpayer and the state tax authority, ensuring that the appointed representative can effectively manage the taxpayer’s obligations.

The Illinois Form PTAX-1000, Power of Attorney, serves a similar function to the Iowa IA 2848 form. It allows taxpayers to appoint a representative to handle their tax matters with the Illinois Department of Revenue. This form requires the same basic information about the taxpayer and representative and specifies the tax types involved. Both forms aim to streamline the process of tax representation, ensuring that taxpayers can receive assistance in managing their obligations.

The Michigan Form 151, Power of Attorney, is another document that resembles the Iowa IA 2848 form. This Michigan form permits taxpayers to authorize a representative to act on their behalf for tax purposes. It requires detailed information about both the taxpayer and the representative, similar to the Iowa form. Both forms provide the appointed representative with the authority to access confidential tax information and represent the taxpayer in communications with the respective state tax authority, facilitating a more efficient resolution of tax matters.

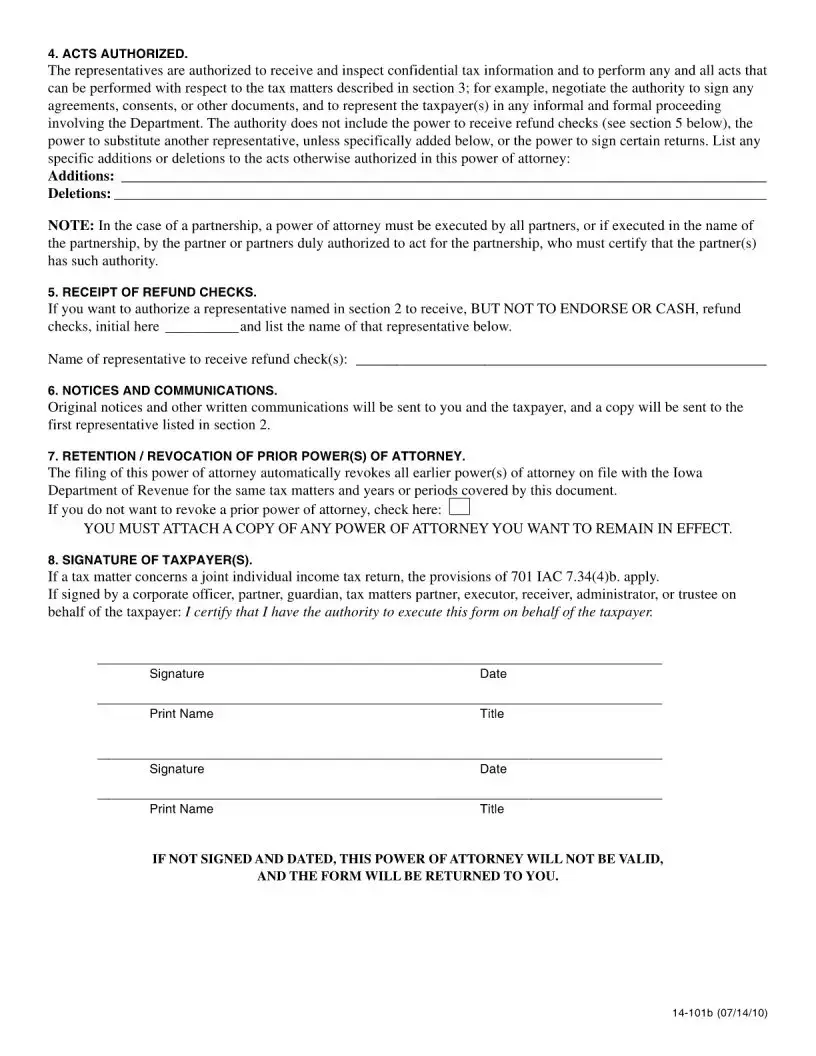

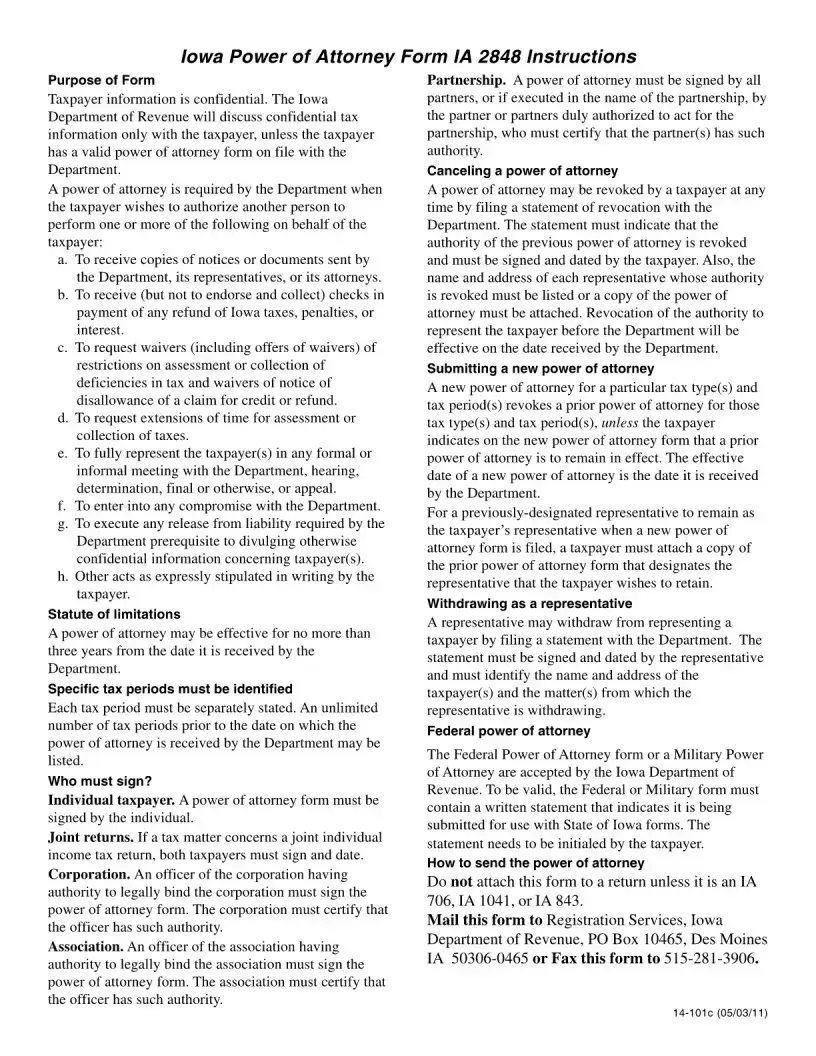

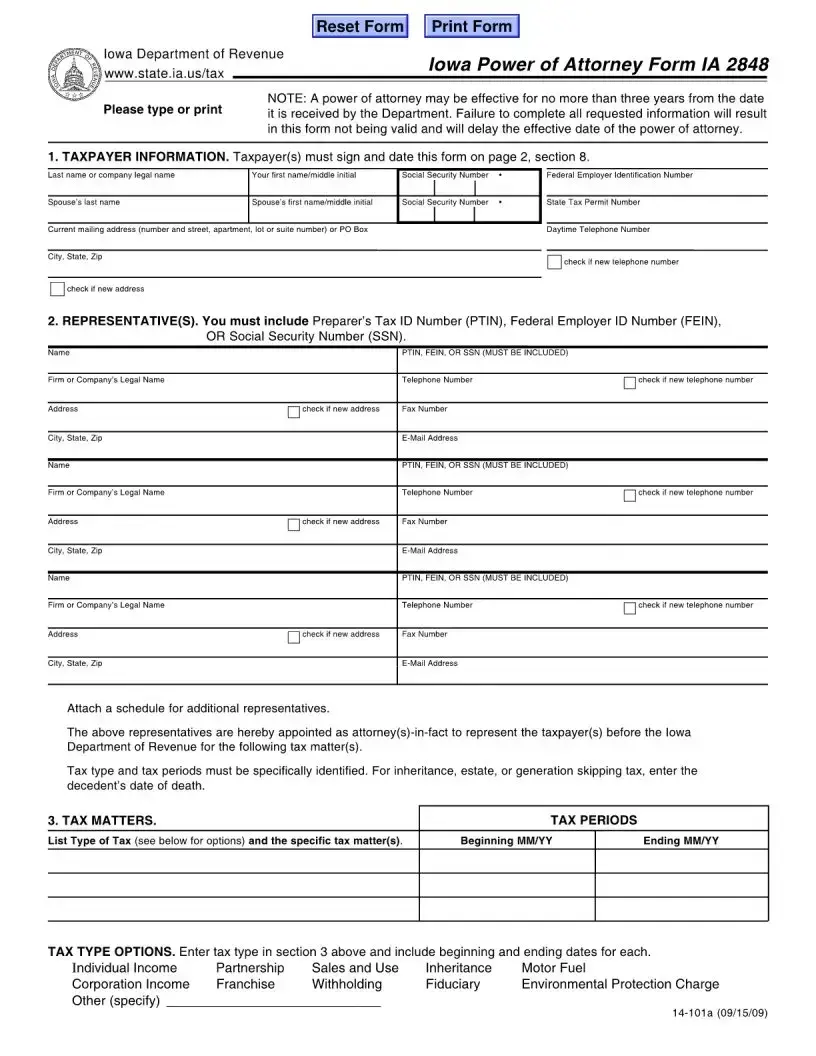

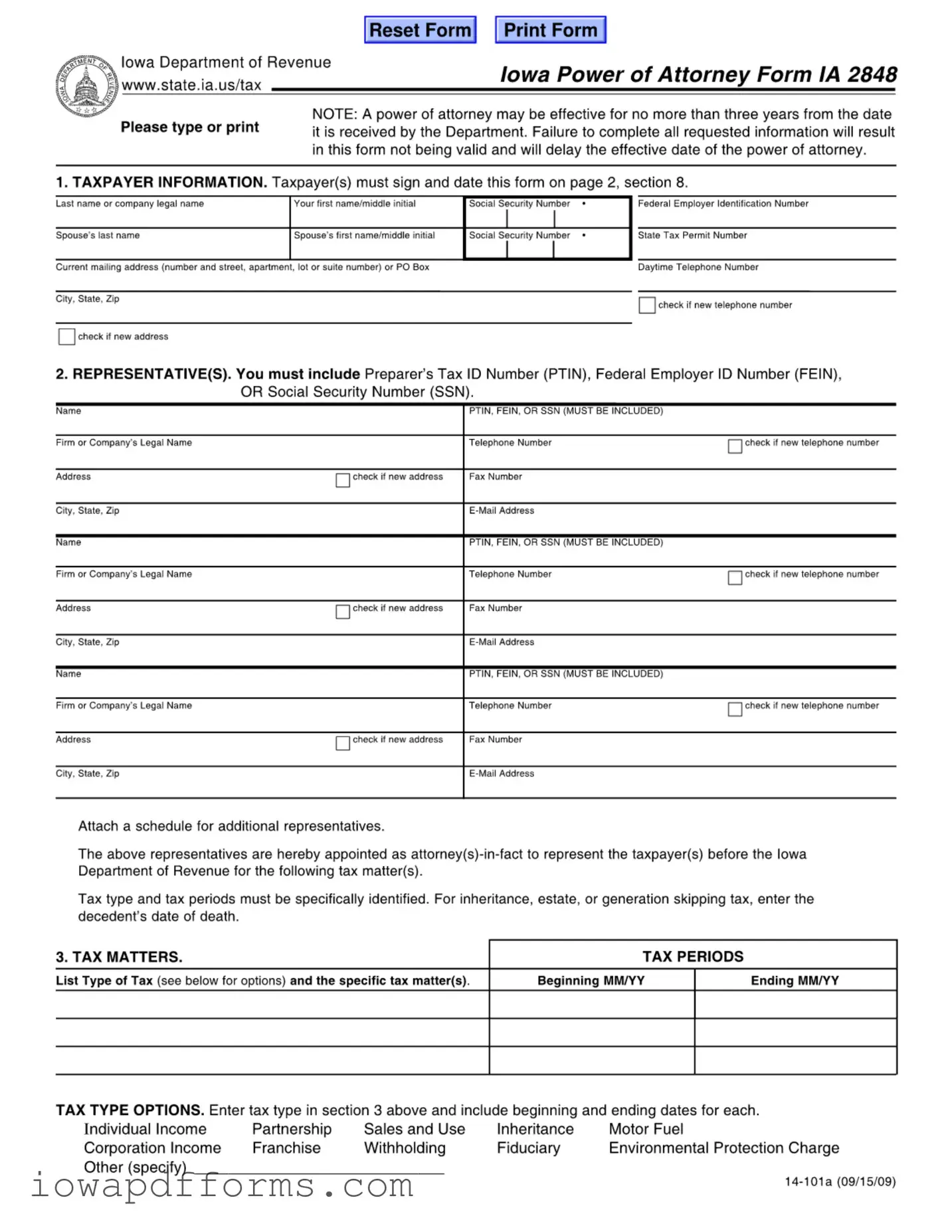

The Iowa IA 2848 form serves as a Power of Attorney, allowing a designated representative to act on behalf of a taxpayer in tax matters. Along with this form, several other documents may be necessary to ensure comprehensive representation and compliance with tax regulations. Below is a list of documents commonly used alongside the IA 2848 form.

Each of these forms plays a crucial role in ensuring compliance with Iowa tax laws. Properly completing and submitting these documents can help facilitate a smoother tax process for individuals and businesses alike.

When filling out the Iowa IA 2848 form, consider the following dos and don'ts: