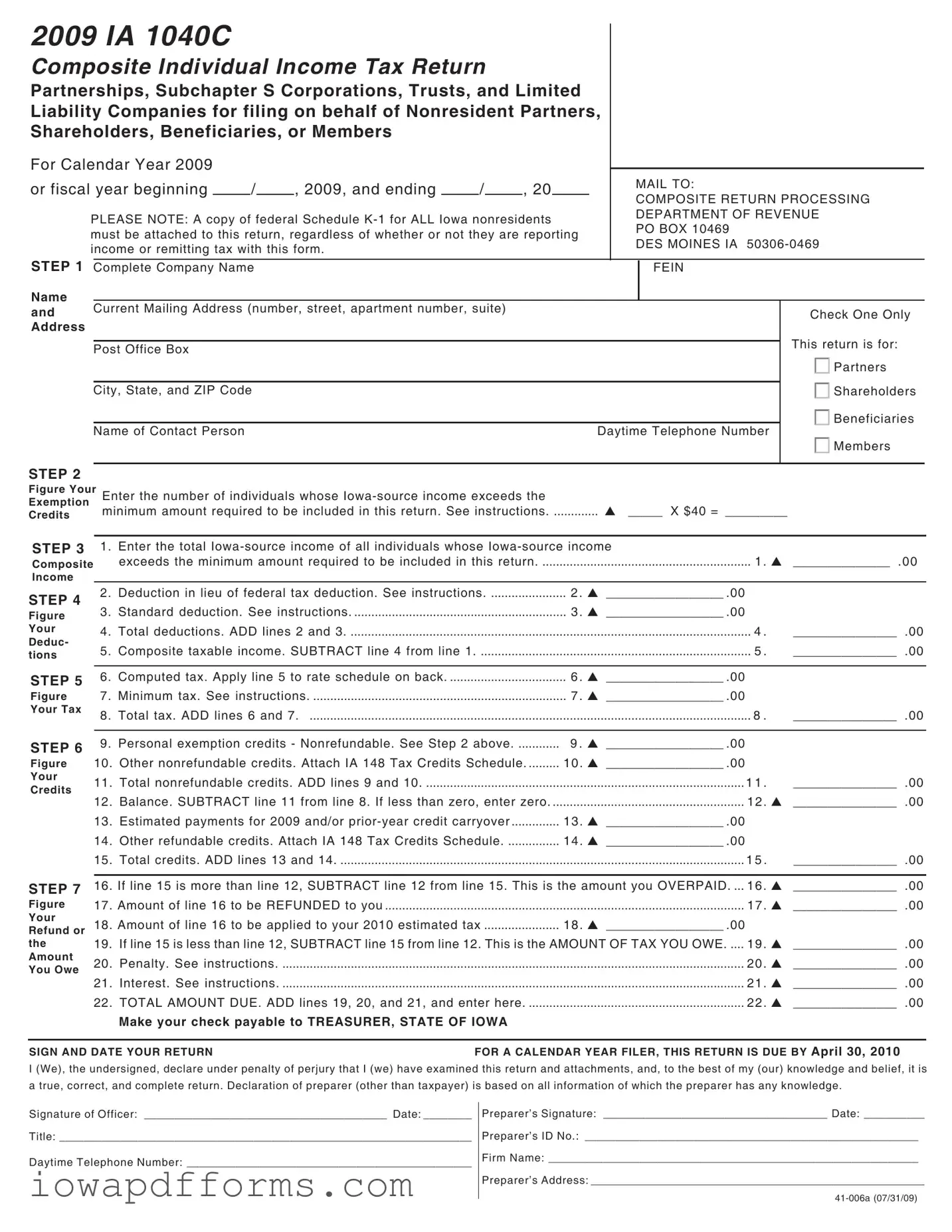

Fill in Your Iowa Ia 1040C Template

Fill in Your Iowa Ia 1040C Template

Iowa Lead Safety - Purchasers are empowered to make informed decisions based on disclosures.

Iowa 470 3361 - The form serves as a guide for fostering awareness of SSI eligibility indicators.

For those looking to ensure a smooth transaction, understanding the importance of a reliable ATV Bill of Sale can be beneficial for both buyers and sellers. A thorough guide on the subject can be accessed through this informative ATV Bill of Sale overview.

Iowa Divorce Forms - Recognize the need for ongoing protection by formally requesting changes to active protective orders.

The Iowa IA 1040C form is similar to the IRS Form 1065, which is used for partnerships. Both forms allow partnerships to report income, deductions, and credits for their members. The IA 1040C is specifically designed for nonresident partners in Iowa, while Form 1065 is used at the federal level. Each form requires detailed reporting of income and deductions, ensuring that all partners are accounted for in the tax calculation. This structure helps streamline the tax process for partnerships, making it easier for nonresident partners to fulfill their tax obligations.

Another document similar to the Iowa IA 1040C is the IRS Form 1120S, which is used by S corporations. Like the IA 1040C, Form 1120S allows S corporations to report their income, deductions, and credits. Both forms require that the income be passed through to shareholders, who then report it on their individual tax returns. The IA 1040C serves nonresident shareholders in Iowa, while Form 1120S serves shareholders at the federal level. This similarity helps maintain consistency in how income is reported and taxed across different types of entities.

The Iowa IA 1040C also resembles the IRS Form 1041, which is used for estates and trusts. Both forms enable the reporting of income generated by the estate or trust, including distributions to beneficiaries. The IA 1040C focuses on nonresident beneficiaries in Iowa, while Form 1041 is applicable at the federal level. Each form requires the attachment of supporting documents, such as K-1s, to ensure accurate reporting of income and tax obligations. This parallel allows for a streamlined process for beneficiaries receiving income from estates or trusts.

Form IA 148 is another document related to the Iowa IA 1040C. The IA 148 Tax Credits Schedule is used to report nonrefundable credits that can reduce the tax owed. Both forms require accurate reporting of credits to ensure compliance with state tax regulations. The IA 148 must be attached to the IA 1040C to provide a complete picture of the taxpayer's credits. This connection between the two forms helps ensure that taxpayers receive any credits they are entitled to while filing their composite return.

The Iowa IA 1040C is also similar to the IRS Form 1040NR, which is used by nonresident aliens. Both forms are designed for individuals who do not reside in the state or country where they earn income. The IA 1040C allows nonresident partners and shareholders to report Iowa-source income, while Form 1040NR focuses on U.S. source income. Each form provides a way for nonresidents to fulfill their tax obligations while ensuring they are taxed only on income sourced from the respective jurisdiction.

For those considering a transaction involving trailers, completing a Trailer Bill of Sale form is essential to ensure a clear transfer of ownership. This legal document, which records the sale and outlines vital details of the trailer, is crucial for both buyers and sellers. To learn more about this form and its importance in facilitating smooth transactions, visit https://billofsaleforvehicles.com/editable-trailer-bill-of-sale.

Lastly, the Iowa IA 1040 is a relevant document. This form is used by residents to report their individual income tax. While the IA 1040C is specifically for nonresidents and composite returns, both forms share similar structures in terms of income reporting, deductions, and credits. The IA 1040C is tailored to accommodate the unique needs of nonresidents, while the IA 1040 is for residents. This distinction helps maintain clarity in tax reporting for individuals based on their residency status.

When filing the Iowa IA 1040C form, there are several other documents that may be required to ensure a complete and accurate submission. Each of these forms serves a specific purpose and can help streamline the process. Here’s a brief overview of four important documents often used alongside the IA 1040C.

Having these documents ready and correctly filled out can significantly ease the filing process for the IA 1040C. It’s always a good idea to double-check that everything is in order to avoid any delays or issues with your tax return.

When filling out the Iowa IA 1040C form, it is crucial to ensure accuracy and compliance. Here are five essential dos and don’ts to consider:

2009 IA 1040C

Composite Individual Income Tax Return

Partnerships, Subchapter S Corporations, Trusts, and Limited

Liability Companies for filing on behalf of Nonresident Partners,

Shareholders, Beneficiaries, or Members

For Calendar Year 2009 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MAIL TO: |

||

or fiscal year beginning |

|

/ |

|

, 2009, and ending |

|

/ |

|

, 20 |

|

|

||

|

|

|

|

|

|

COMPOSITE RETURN PROCESSING |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

PLEASE NOTE: A copy of federal Schedule |

|

DEPARTMENT OF REVENUE |

||||||||||

|

PO BOX 10469 |

|||||||||||

must be attached to this return, regardless of whether or not they are reporting |

|

|||||||||||

|

DES MOINES IA |

|||||||||||

income or remitting tax with this form. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||

STEP 1 Complete Company Name |

|

|

|

|

|

|

|

|

FEIN |

|||

Name

and Current Mailing Address (number, street, apartment number, suite)Check One Only

Address

Post Office Box |

|

This return is for: |

|||

|

|

|

|

|

|

|

|

|

|

|

Partners |

|

|

|

|

|

|

City, State, and ZIP Code |

|

|

|

|

Shareholders |

|

|

|

|

|

Beneficiaries |

|

|

|

|

|

|

|

|

|

|

|

|

Name of Contact Person |

Daytime Telephone Number |

|

|

||

|

|||||

|

|

|

|

|

Members |

STEP 2

Figure Your

Exemption

Credits

Enter the number of individuals whose |

|

minimum amount required to be included in this return. See instructions |

_____ X $40 = _________ |

STEP 3 |

1. Enter the total |

|

|

Composite |

exceeds the minimum amount required to be included in this return |

1 . |

______________ . 00 |

Income

STEP 4

Figure Your Deduc- tions

STEP 5

Figure Your Tax

STEP 6

Figure

Your

Credits

STEP 7

Figure Your Refund or the Amount You Owe

2. |

Deduction in lieu of federal tax deduction. See instructions |

2 . |

_________________ .00 |

|

|

|

3. |

Standard deduction. See instructions |

3 . |

_________________ .00 |

|

|

|

4. |

Total deductions. ADD lines 2 and 3 |

|

4 . |

_______________ |

.00 |

|

5. |

Composite taxable income. SUBTRACT line 4 from line 1 |

|

5 . |

_______________ |

.00 |

|

|

|

|

|

|

|

|

6. |

Computed tax. Apply line 5 to rate schedule on back |

6 . |

_________________ .00 |

|

|

|

7. |

Minimum tax. See instructions |

7 . |

_________________ .00 |

|

|

|

8. |

Total tax. ADD lines 6 and 7. ................................................................................................................................. 8 . |

_______________ |

.00 |

|||

|

|

|

|

|

|

|

9. |

Personal exemption credits - Nonrefundable. See Step 2 above |

9 . |

_________________ .00 |

|

|

|

10. |

Other nonrefundable credits. Attach IA 148 Tax Credits Schedule |

10 . _________________ .00 |

|

|

|

|

11. |

Total nonrefundable credits. ADD lines 9 and 10 |

|

1 1 . |

_______________ |

.00 |

|

12. |

Balance. SUBTRACT line 11 from line 8. If less than zero, enter zero |

|

12 . |

_______________ |

.00 |

|

13. |

Estimated payments for 2009 and/or |

13 . _________________ .00 |

|

|

|

|

14. |

Other refundable credits. Attach IA 148 Tax Credits Schedule |

14 . _________________ .00 |

|

|

|

|

15. |

Total credits. ADD lines 13 and 14 |

|

1 5 . |

_______________ |

.00 |

|

|

|

|

|

|

||

16. |

If line 15 is more than line 12, SUBTRACT line 12 from line 15. This is the amount you OVERPAID. ... |

16 . |

_______________ |

.00 |

||

17. |

Amount of line 16 to be REFUNDED to you |

|

17 . |

_______________ .00 |

||

18. |

Amount of line 16 to be applied to your 2010 estimated tax |

18 . _________________ .00 |

|

|

|

|

19. |

If line 15 is less than line 12, SUBTRACT line 15 from line 12. This is the AMOUNT OF TAX YOU OWE |

19 . |

_______________ |

.00 |

||

20. |

Penalty. See instructions |

|

20 . |

_______________ |

.00 |

|

21. |

Interest. See instructions |

|

21 . |

_______________ |

.00 |

|

22. |

TOTAL AMOUNT DUE. ADD lines 19, 20, and 21, and enter here |

|

22 . |

_______________ .00 |

||

|

Make your check payable to TREASURER, STATE OF IOWA |

|

|

|

|

|

SIGN AND DATE YOUR RETURN |

FOR A CALENDAR YEAR FILER, THIS RETURN IS DUE BY April 30, 2010 |

I (We), the undersigned, declare under penalty of perjury that I (we) have examined this return and attachments, and, to the best of my (our) knowledge and belief, it is a true, correct, and complete return. Declaration of preparer (other than taxpayer) is based on all information of which the preparer has any knowledge.

Signature of Officer: ________________________________________ Date: ________

Title: ____________________________________________________________________

Daytime Telephone Number: _______________________________________________

Preparer’s Signature: _____________________________________ Date: __________

Preparer’s ID No.: _______________________________________________________

Firm Name: _____________________________________________________________

Preparer’s Address: _______________________________________________________

Instructions for Composite Iowa Individual Income Tax Return

Election of Composite Filing

Composite returns for the 2009 calendar year must be filed by April 30, 2010. An automatic

Filing Requirements

Nonresident partners, shareholders, members, or beneficiaries cannot be included in a composite return if the nonresident does not have more income from Iowa sources than the amount of one standard deduction for a single taxpayer plus an amount of income necessary to create a tax liability at the effective tax rate on the composite return sufficient to offset one personal exemption. See minimum filing requirements below under line 6.

In addition, the above individuals should not be included if they have incomes from Iowa sources other than from the partnership or other entity; these individuals are required to file Iowa individual income tax returns.

Line Instructions

1.Each nonresident partner’s, shareholder’s, or member’s Iowa

IA 1040C.

Beneficiaries of a trust do not have an Iowa

2.A deduction is allowed in lieu of the deduction for federal tax paid and is based upon the following schedule:

Amount shown on line 1 |

|

Deduction |

||

0 |

- |

$49,999 = |

No deduction |

|

$50,000 |

- |

$99,999 |

= |

5% of line 1 |

$100,000 |

- |

$199,999 |

= |

10% of line 1 |

Over |

$200,000 |

= |

15% of line 1 |

|

3.For 2009 the standard deduction allowed is the lesser of $1,780 or the income attributable to Iowa of the partner, shareholder, or member filing this composite return.

|

|

TAX RATE SCHEDULE |

|

|

|

|

|

|

|

But |

|

|

|

|

Of Excess |

Minimum |

Over |

Not Over |

|

|

Tax Rate |

|

Over |

Income |

$0 |

$1,407 |

$0.00 |

+ |

(0.36% |

x |

$0) |

Filing |

$1,407 |

$2,814 |

$5.07 |

+ |

(0.72% |

x |

$1,407) |

Requirement |

$2,814 |

$5,628 |

$15.20 |

+ |

(2.43% |

x |

$2,814) |

$2,669 |

$5,628 |

$12,663 |

$83.58 |

+ |

(4.50% |

x |

$5,628) |

$2,434 |

$12,663 |

$21,105 |

$400.16 |

+ |

(6.12% |

x |

$12,663) |

$2,397 |

$21,105 |

$28,140 |

$916.81 |

+ |

(6.48% |

x |

$21,105) |

$2,368 |

$28,140 |

$42,210 |

$1,372.68 |

+ |

(6.80% |

x |

$28,140) |

$2,285 |

$42,210 |

$63,315 |

$2,329.44 |

+ |

(7.92% |

x |

$42,210) |

$2,225 |

$63,315 |

over |

$4,000.96 |

+ |

(8.98% |

x |

$63,315) |

|

|

|

|

|

|

|

|

6.Use the tax rate schedule above to figure your tax on composite Iowa taxable income. Also listed are the minimum requirements for each tax rate.

7.Partners, shareholders, or members reporting income on the composite return may also be subject to Iowa minimum tax. The Iowa alternative minimum tax is imposed on most of the same tax preference and adjustment items treated as exclusions as for federal alternative minimum tax purposes. Please see form IA 6251 to determine if any Iowa minimum tax is due, and attach completed form if necessary.

9.Personal exemption credits for 2009 for each partner, shareholder or member is $40.

10.Enter the total of the nonrefundable credits from the IA 148 Tax Credits Schedule. The IA 148 Tax Credits Schedule must be attached.

13.Enter the total amount of 2009 estimated tax payments and any of the prior year’s refund applied to your estimated payments for 2009.

Although estimated payments are not required, 2010 estimated payments may be made on form IA 1040ES using the partnership’s, limited liability company’s, S corporation’s, or trust’s identification number.

14.Enter the total of the refundable credits from the IA 148 Tax Credits Schedule. Attach the IA 148 Tax Credits Schedule.

20.If you do not mail your return by the due date and at least 90% of the correct tax is not paid, you owe an additional 10% of the tax due. If you file your return on time but do not pay at least 90% of the correct tax due, you owe an additional 5% of the tax due.

21.Interest is added at a rate of 0.4% per month beginning on the due date of the return and accrues each month until payment is made.

Preparer’s ID Number

Enter preparer’s SSN, FEIN, or PTIN.