Fill in Your Iowa 44 017B Template

Fill in Your Iowa 44 017B Template

Iowa 470 0040 - It is necessary to include the state ID on the form for accurate processing.

When preparing to enter into a real estate transaction, it is crucial to utilize the correct documentation to facilitate the process, and the Texas TREC Residential Contract form is indispensable in this regard. This essential document provides clarity in the sale of residential properties by detailing the terms agreed upon by both the buyer and seller. For more information and resources related to this important form, you can visit Texas Documents.

Resale Certificate Verification - Certificate accuracy is legally binding; any false information can lead to penalties.

The Iowa 44 017B form, known as the Nonresident Claim For Release From Withholding, shares similarities with the IRS Form W-8BEN. Both documents serve to establish the tax status of nonresident individuals and entities. The W-8BEN is used by non-U.S. residents to certify their foreign status and claim any applicable tax treaty benefits. Like the Iowa form, it allows individuals to avoid unnecessary withholding on income they receive from U.S. sources. Both forms require the individual to provide personal information and certify their eligibility for tax exemptions or reduced withholding rates.

If you're looking to sell a trailer, it’s important to properly document the transaction with a Trailer Bill of Sale form. This legal document not only captures the details of the sale but also serves as proof of purchase. For more information on how to create this essential form, visit billofsaleforvehicles.com/editable-trailer-bill-of-sale/.

Another document similar to the Iowa 44 017B is the IRS Form 1040NR, which is the U.S. Nonresident Alien Income Tax Return. This form is used by nonresident aliens to report their income earned in the United States. Just as the Iowa form allows nonresidents to claim a release from withholding, the 1040NR enables them to report their income and calculate their tax liability. Both forms require detailed information about income sources and may involve calculations that determine whether withholding is necessary.

The Iowa 44 017B also resembles the IRS Form 8833, which is used to disclose a treaty-based return position. This form is relevant for nonresidents who claim a tax treaty benefit that may exempt them from certain U.S. taxes. Similar to the Iowa form, it requires individuals to provide information about their income and the treaty provisions they are invoking. Both documents facilitate the process of claiming exemptions from withholding based on specific eligibility criteria.

Another related document is the Iowa IA 1040ES voucher. This form is utilized by individuals making estimated tax payments to the state of Iowa. Like the Iowa 44 017B, it allows taxpayers to manage their tax obligations proactively rather than relying solely on withholding. Both forms require payment calculations based on anticipated income, and they help ensure that taxpayers fulfill their tax responsibilities in a timely manner.

The IRS Form 1099-MISC is also similar to the Iowa 44 017B. This form is used to report various types of income received by nonemployees, including nonresident aliens. While the Iowa form addresses withholding exemptions, the 1099-MISC provides information to both the payer and the recipient about the income that has been paid. Both documents are essential for ensuring compliance with tax reporting requirements and help clarify the tax obligations of nonresident recipients.

Additionally, the IRS Form 1042-S is relevant in this context, as it is used to report income paid to nonresident aliens and the withholding that has been applied. Like the Iowa 44 017B, it addresses the tax implications of payments made to nonresidents. Both forms ensure that the correct amount of tax is withheld or reported, helping to prevent misunderstandings between payers and recipients regarding tax liabilities.

The Iowa 44 017B also has parallels with the IRS Form 8288, which is used for withholding tax on dispositions of U.S. real property interests by foreign persons. Both forms deal with withholding tax obligations for nonresidents, albeit in different contexts. They both require the payer to assess their withholding responsibilities based on the nonresident's tax status and the nature of the income being paid.

Lastly, the Iowa IA 1040 form is similar to the Iowa 44 017B in that it is a tax return form for residents and nonresidents alike. While the IA 1040 is primarily for residents, nonresidents who have income sourced from Iowa may also need to file it. Both forms require the taxpayer to provide detailed information about their income and expenses, and both are crucial for determining the correct tax obligations to the state of Iowa.

The Iowa 44 017B form is essential for nonresidents who wish to request a release from withholding on Iowa nonwage income. Alongside this form, there are several other documents that may be necessary to complete the process effectively. Understanding these forms can help ensure compliance and facilitate smoother interactions with the Iowa Department of Revenue.

Each of these documents plays a crucial role in the tax process for nonresidents in Iowa. It is important to gather and complete them accurately to ensure compliance and avoid potential issues with tax withholding and reporting. For further assistance, reaching out to the Iowa Department of Revenue can provide clarity and guidance.

When filling out the Iowa 44 017B form, it's important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of what to do and what to avoid:

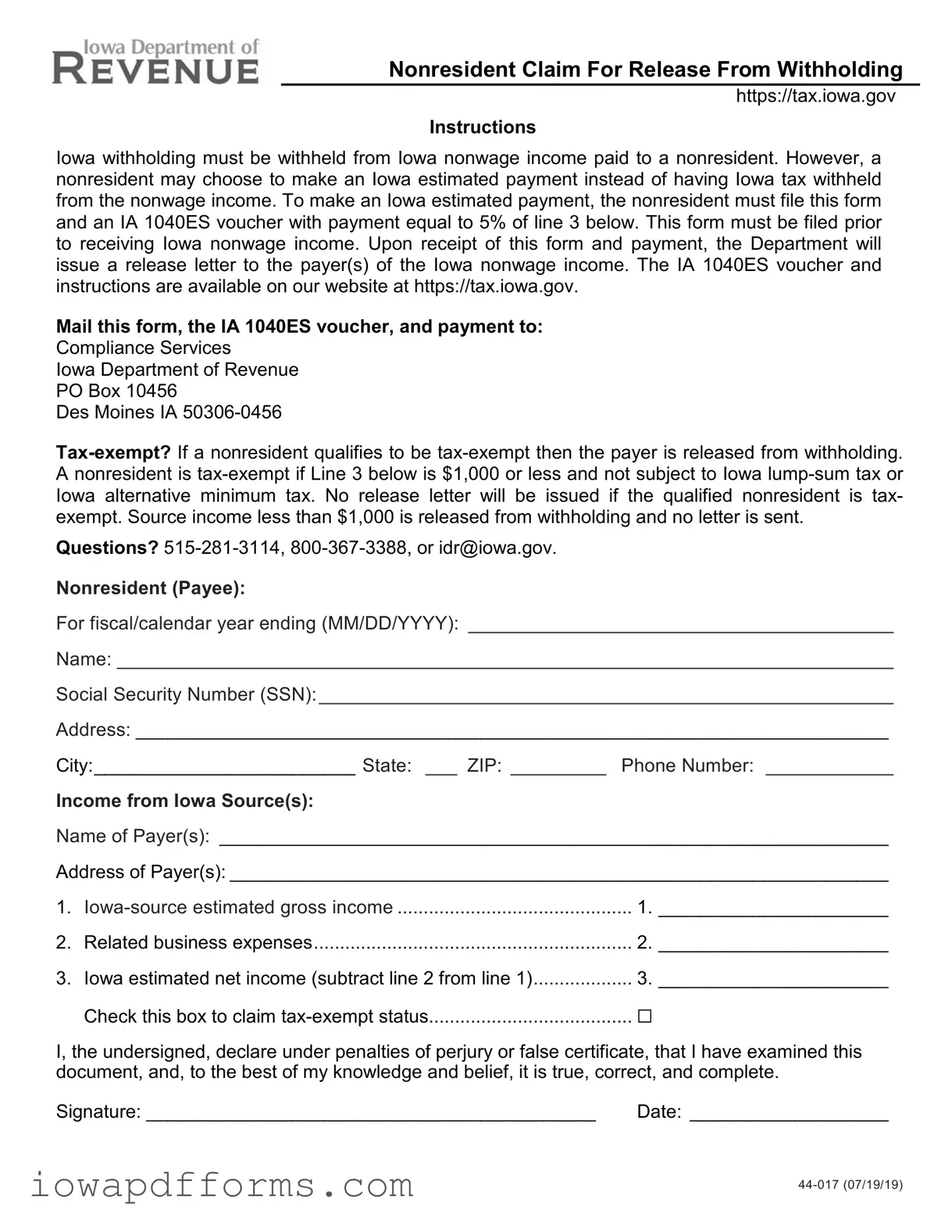

Nonresident Claim For Release From Withholding

https://tax.iowa.gov

Instructions

Iowa withholding must be withheld from Iowa nonwage income paid to a nonresident. However, a nonresident may choose to make an Iowa estimated payment instead of having Iowa tax withheld from the nonwage income. To make an Iowa estimated payment, the nonresident must file this form and an IA 1040ES voucher with payment equal to 5% of line 3 below. This form must be filed prior to receiving Iowa nonwage income. Upon receipt of this form and payment, the Department will issue a release letter to the payer(s) of the Iowa nonwage income. The IA 1040ES voucher and instructions are available on our website at https://tax.iowa.gov.

Mail this form, the IA 1040ES voucher, and payment to:

Compliance Services

Iowa Department of Revenue

PO Box 10456

Des Moines IA

Questions?

Nonresident (Payee):

For fiscal/calendar year ending (MM/DD/YYYY): ________________________________________

Name: _________________________________________________________________________

Social Security Number (SSN):______________________________________________________

Address: ________________________________________________________________________

City:_________________________ State: ___ ZIP: _________ Phone Number: ____________

Income from Iowa Source(s):

Name of Payer(s): ________________________________________________________________

Address of Payer(s): _______________________________________________________________

1. |

1. ______________________ |

|

2. |

Related business expenses |

2. ______________________ |

3. |

Iowa estimated net income (subtract line 2 from line 1) |

3. ______________________ |

|

Check this box to claim |

☐ |

I, the undersigned, declare under penalties of perjury or false certificate, that I have examined this document, and, to the best of my knowledge and belief, it is true, correct, and complete.

Signature: ___________________________________________ |

Date: ___________________ |