Fill in Your Ia 706 Iowa Template

Fill in Your Ia 706 Iowa Template

Iowa Lead Safety - It highlights the risks associated with lead-based paint and potential hazards.

Iowa 470 4299 - The verification process helps streamline approvals for necessary medical services.

When preparing to draft your Indiana Promissory Note, it's important to familiarize yourself with the necessary details and legal requirements, which you can explore further at https://promissoryform.com, ensuring that your agreement is thorough and binding.

Iowa Divorce Forms - This is a formal request to obtain a Protective Order after a domestic abuse case has been adjudicated.

The IA 706 Iowa Inheritance Tax Return shares similarities with the federal Form 706, which is used for federal estate tax purposes. Both forms require detailed information about the decedent's estate, including assets and liabilities. They also involve calculations to determine the total value of the estate and any taxes owed. While the IA 706 focuses specifically on Iowa inheritance tax, the federal Form 706 assesses federal estate tax, making it crucial for executors to understand both to ensure compliance with state and federal laws.

Another document that resembles the IA 706 is the Illinois Form 700, which is the Illinois Estate Tax Return. Like the IA 706, this form collects information about the decedent's assets and calculates the estate tax owed to the state. Both forms require an inventory of property and debts, and they involve similar processes for determining the net estate. The key difference lies in the specific tax laws and exemptions applicable in each state, which executors must navigate carefully.

The New York State Estate Tax Return (Form ET-706) is also comparable to the IA 706. Both documents require a comprehensive listing of the decedent's assets and liabilities. They also necessitate the calculation of the estate tax based on the net estate value. In New York, the estate tax can be influenced by the size of the estate, while Iowa's tax structure may differ. Understanding these nuances is essential for executors managing estates in either state.

To effectively navigate the complexities of real estate transactions, it is important to familiarize yourself with all relevant documents, including the Texas TREC Residential Contract form. Resources such as Texas Documents can provide valuable assistance in understanding the necessary forms and ensuring compliance with state regulations.

The California Form 706 is another document that parallels the IA 706. This form is used for reporting estate tax in California, which, unlike Iowa, does not impose an estate tax as of 2023. However, the reporting requirements and the need for detailed asset documentation are similar in both forms. Executors in California must be aware of this distinction, especially when dealing with estates that may have assets in multiple states.

In addition, the Massachusetts Estate Tax Return (Form M-706) is similar to the IA 706. Both forms require an inventory of the decedent's assets and an accounting of any debts. The calculations for the estate tax owed are also a common feature. Massachusetts has its own set of tax thresholds and exemptions, which can significantly impact the final tax liability, making it important for executors to be informed about local regulations.

The Florida Estate Tax Return is another document that shares characteristics with the IA 706. While Florida does not currently impose an estate tax, the return still requires a detailed accounting of the decedent's assets and liabilities. This similarity in documentation is crucial for estates with connections to multiple states, as it helps ensure that all relevant information is captured for tax purposes.

The Pennsylvania Inheritance Tax Return is yet another form that resembles the IA 706. Both require a thorough listing of the decedent’s assets and liabilities, as well as calculations for the inheritance tax owed. Pennsylvania's inheritance tax rates and exemptions differ from Iowa's, but the overall structure of the forms is quite similar, making it essential for executors to understand the specifics of each state's requirements.

Lastly, the New Jersey Inheritance Tax Return (Form IT-R) is comparable to the IA 706. Both documents require detailed information about the decedent's estate, including assets, debts, and beneficiary information. The calculation of the tax owed is a shared feature as well. However, the tax rates and exemptions vary significantly between New Jersey and Iowa, so executors must be diligent in understanding the differences to ensure compliance.

When dealing with the IA 706 Iowa Inheritance Tax Return, several additional forms and documents may be necessary to ensure a smooth process. Each of these documents serves a specific purpose and can help clarify various aspects of the estate's administration. Below is a list of common forms that are often used alongside the IA 706.

Gathering these documents can seem daunting, but each plays a vital role in the inheritance tax process. By ensuring that all necessary forms are complete and submitted, the estate can be managed more efficiently, reducing the likelihood of complications down the line.

When filling out the IA 706 Iowa Inheritance Tax Return, it's important to follow specific guidelines. Here are six things you should and shouldn't do:

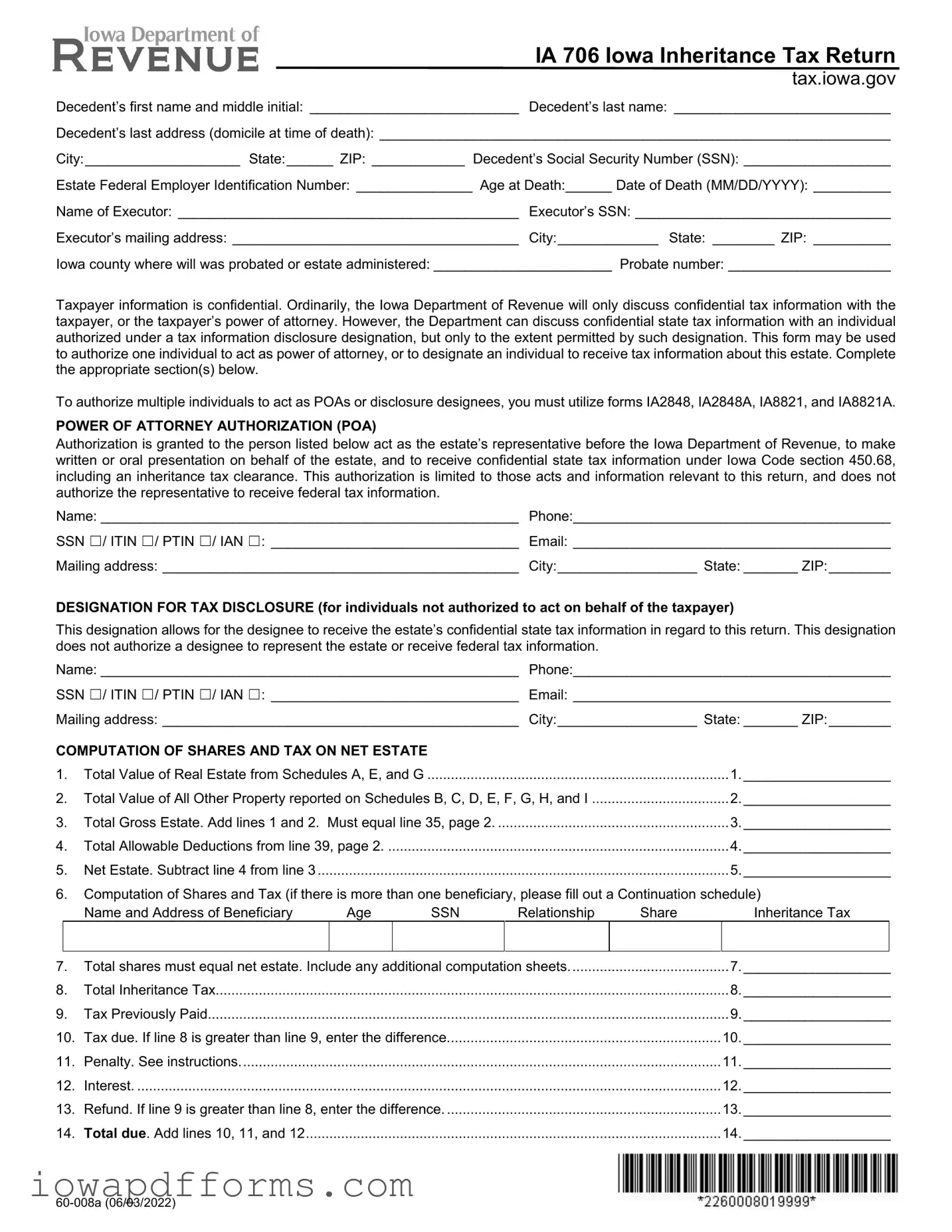

IA 706 Iowa Inheritance Tax Return

tax.iowa.gov

Decedent’s first name and middle initial: ___________________________ Decedent’s last name: ____________________________

Decedent’s last address (domicile at time of death): __________________________________________________________________

City:____________________ State:______ ZIP: ____________ Decedent’s Social Security Number (SSN): ___________________

Estate Federal Employer Identification Number: _______________ Age at Death:______ Date of Death (MM/DD/YYYY): __________

Name of Executor: ____________________________________________ Executor’s SSN: _________________________________

Executor’s mailing address: _____________________________________ City:_____________ State: ________ ZIP: __________

Iowa county where will was probated or estate administered: _______________________ Probate number: _____________________

Taxpayer information is confidential. Ordinarily, the Iowa Department of Revenue will only discuss confidential tax information with the taxpayer, or the taxpayer’s power of attorney. However, the Department can discuss confidential state tax information with an individual authorized under a tax information disclosure designation, but only to the extent permitted by such designation. This form may be used to authorize one individual to act as power of attorney, or to designate an individual to receive tax information about this estate. Complete the appropriate section(s) below.

To authorize multiple individuals to act as POAs or disclosure designees, you must utilize forms IA2848, IA2848A, IA8821, and IA8821A.

POWER OF ATTORNEY AUTHORIZATION (POA)

Authorization is granted to the person listed below act as the estate’s representative before the Iowa Department of Revenue, to make written or oral presentation on behalf of the estate, and to receive confidential state tax information under Iowa Code section 450.68, including an inheritance tax clearance. This authorization is limited to those acts and information relevant to this return, and does not authorize the representative to receive federal tax information.

Name: ______________________________________________________ |

Phone:_________________________________________ |

SSN ☐/ ITIN ☐/ PTIN ☐/ IAN ☐: ________________________________ |

Email: _________________________________________ |

Mailing address: ______________________________________________ |

City:__________________ State: _______ ZIP:________ |

DESIGNATION FOR TAX DISCLOSURE (for individuals not authorized to act on behalf of the taxpayer)

This designation allows for the designee to receive the estate’s confidential state tax information in regard to this return. This designation does not authorize a designee to represent the estate or receive federal tax information.

Name: ______________________________________________________ |

Phone:_________________________________________ |

||

SSN ☐/ ITIN ☐/ PTIN ☐/ IAN ☐: ________________________________ |

Email: _________________________________________ |

||

Mailing address: ______________________________________________ |

City:__________________ State: _______ ZIP:________ |

||

COMPUTATION OF SHARES AND TAX ON NET ESTATE |

|

|

|

1. |

Total Value of Real Estate from Schedules A, E, and G |

1.___________________ |

|

2. |

Total Value of All Other Property reported on Schedules B, C, D, E, F, G, H, and I |

2.___________________ |

|

3. |

Total Gross Estate. Add lines 1 and 2. Must equal line 35, page 2 |

3.___________________ |

|

4. |

Total Allowable Deductions from line 39, page 2 |

4.___________________ |

|

5. |

Net Estate. Subtract line 4 from line 3 |

5.___________________ |

|

6.Computation of Shares and Tax (if there is more than one beneficiary, please fill out a Continuation schedule)

|

|

Name and Address of Beneficiary |

Age |

SSN |

Relationship |

Share |

|

Inheritance Tax |

|

|

|

|

|

|

|

|

|

7. |

Total shares must equal net estate. Include any additional computation sheets |

|

7. |

___________________ |

||||

8. |

Total Inheritance Tax |

|

|

|

|

8. |

___________________ |

|

9. |

Tax Previously Paid |

|

|

|

|

9. |

___________________ |

|

10. |

Tax due. If line 8 is greater than line 9, enter the difference |

|

|

10. |

___________________ |

|||

11. |

Penalty. See instructions |

|

|

|

|

11. |

___________________ |

|

12. |

Interest |

|

|

|

|

12. |

___________________ |

|

13. |

Refund. If line 9 is greater than line 8, enter the difference |

|

|

13. |

___________________ |

|||

14. |

Total due. Add lines 10, 11, and 12 |

|

|

|

|

14. |

___________________ |

|

IA 706, page 2

15. |

Marital status of decedent at death: Married ☐ |

Widow(er) ☐ |

Single ☐ |

Divorced ☐ |

|

|

|

|||

|

The relationship of decedent’s children to surviving spouse must be included if decedent died intestate. |

|

|

|

||||||

16. |

Were any children born to or adopted by the decedent after execution of the last will? |

|

|

Yes ☐ |

No ☐ |

|||||

|

In all cases of adoption, include a copy of the decree. |

|

|

|

|

|

|

|

|

|

17. |

Decedent’s occupation before death: __________________________________________________________________________ |

|||||||||

18. |

Decedent died: Intestate (include heirship chart) |

☐ |

Estate has trust (include trust agreement) |

☐ |

|

|||||

|

Testate (include copy of will) |

☐ |

|

|

|

|

|

|

|

|

19. |

Election of spouse. Submit copy of election: Under will ☐ |

Distributive share ☐ |

|

|

|

|

|

|

||

20. |

Was a disclaimer filed? If yes, submit copy of disclaimer |

|

|

|

|

Yes ☐ |

No ☐ |

|||

21. |

Do you elect the special use valuation? |

|

|

|

|

|

Yes ☐ |

No ☐ |

||

22. |

Was a federal estate tax return filed? If yes, submit copy |

|

|

|

|

Yes ☐ |

No ☐ |

|||

23. |

Do you elect to claim qualified terminal interest property (QTIP) under Iowa Code 450.3(7) and Internal Revenue |

|

||||||||

|

Code (IRC) section 2056(b)(7)(B)? If yes, include copy of Schedule M of federal estate tax return |

....................... |

Yes ☐ |

No ☐ |

||||||

24. |

Do you elect to pay the federal estate tax in installments as described in IRC section 6166? |

Yes ☐ |

No ☐ |

|||||||

25. |

Do you elect the alternate valuations under Iowa Code section 450.37 (IRC section 2032)? |

Yes ☐ |

No ☐ |

|||||||

Summary of Gross Estate |

|

|

|

|

|

Alternate |

|

Value at Date |

||

Include applicable schedules only. Federal schedules may be used in place of Iowa schedules. |

Value |

|

|

of Death |

||||||

26. |

Real Estate, from Schedule A |

|

|

26. |

|

|

|

|

|

|

27. |

Stocks and Bonds, from Schedule B |

|

|

27. |

|

|

|

|

|

|

28. |

Mortgages, Notes, and Cash, from Schedule C |

|

|

28. |

|

|

|

|

|

|

29. |

....................Insurance on Decedent’s Life, from Schedule D. Include federal form(s) 712 |

29. |

|

|

|

|

|

|||

30. |

Jointly Owned Property, from Schedule E |

|

|

30. |

|

|

|

|

|

|

31. |

Other Miscellaneous Property, from Schedule F |

|

|

31. |

|

|

|

|

|

|

32. |

.........................................................Transfers During Decedent’s Life, from Schedule G. |

|

|

32. |

|

|

|

|

|

|

33. |

Powers of Appointment, from Schedule H |

|

|

33. |

|

|

|

|

|

|

34. |

.........................................Annuities, Section 529 plans, and ABLE plans from Schedule I |

|

34. |

|

|

|

|

|

||

35. |

. ................Total Gross Estate. Add lines 26 through 34. Enter here and on page 1, line 3 |

35. |

|

|

|

|

|

|||

Summary of Deductions – Include Schedules J and K. |

|

|

|

|

|

|

|

|

|

|

36. |

Funeral and Administrative expenses, from Schedule J |

|

|

|

36.___________________ |

|||||

37. |

Debts of Decedent, from Schedule K, part I |

|

|

|

|

37.___________________ |

||||

38. |

Iowa Mortgages and Liens, from Schedule K, part II |

|

|

|

|

38.___________________ |

||||

39. |

Total Deductions. Add lines 36 through 38. Enter here and on page 1, line 4 |

|

39.___________________ |

|||||||

For the Summary of Real and Personal Property Located Outside of Iowa not included in Lines

Summary of Real and Personal Property Located Outside of Iowa Schedule |

|

40. Add all real and personal property items located outside of Iowa as listed on the Summary Statement |

$___________________ |

I, the undersigned, declare under penalties of perjury or false certificate, that I have examined this return, and, to the best of my knowledge and belief, it is true, correct, and complete.

Signature: _________________________________ Capacity or Title: ____________________________________ Date:__________

Preparer’s signature: ________________________ PTIN: ______________________ Phone: ________________ Date:__________

Make checks payable to Iowa Department of Revenue. When you pay by check, you authorize the Department of Revenue to convert your check to a

Mail to: Fiduciary/Inheritance Section

Iowa Department of Revenue

PO Box 10467

Des Moines IA